Snow events are one of the fastest ways property risk changes without showing up in underwriting models. Within days of a winter storm, roof loads increase, drainage systems fail, and freeze thaw cycles accelerate structural wear. Yet many insurance underwriting and risk teams are still making portfolio decisions based on desk reviews, pre storm property data, and imagery that no longer reflects current conditions.

This creates a critical gap in insurance underwriting risk assessment. Post storm property condition verification is often missing, even though snow related exposure can materially increase loss probability across residential and commercial portfolios. Without current, on site property condition data, underwriting teams are left relying on assumptions rather than verified risk indicators.

Snow does not just impact claims. It challenges how insurers evaluate property risk in real time.

Why Snow Events Increase Insurance Underwriting Risk

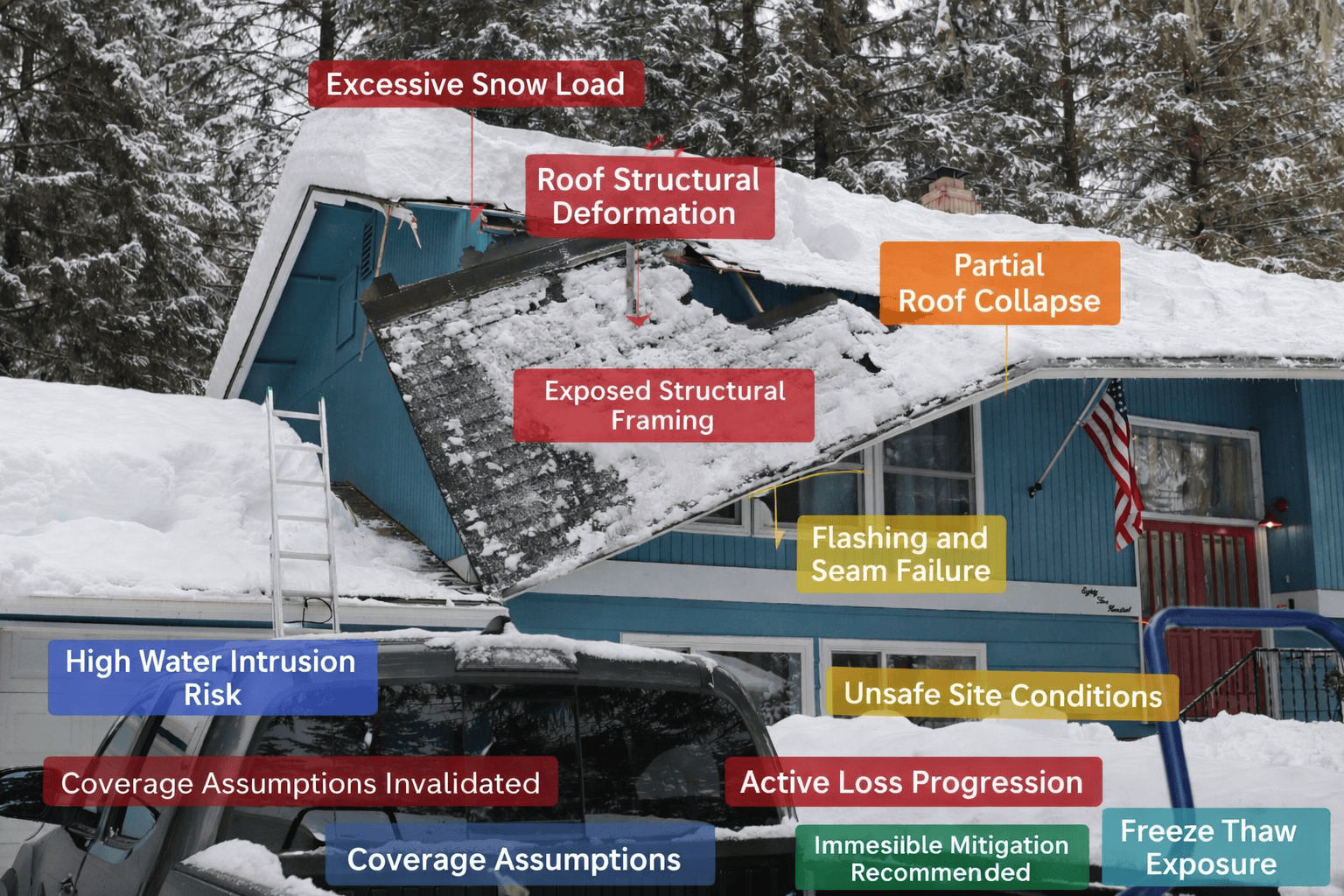

Snow events create dynamic conditions that traditional underwriting processes were never designed to capture. Snow load accumulates unevenly. Ice dams form days after the storm. Drainage failures and mechanical exposure often emerge during thaw cycles, not at first impact.

For insurance underwriting teams managing large portfolios, these changes represent hidden exposure. What looked acceptable before the storm may now exceed risk thresholds, especially for aging properties, flat roofs, or locations with deferred maintenance.

Why Desk Reviews Fail for Post Snow Property Risk Assessment

Desk reviews depend on static data sources. After a snow event, those sources quickly lose relevance.

Common limitations include:

Pre storm inspection reports

Third party imagery captured months earlier

Satellite or street level images that cannot show roof load or ice buildup

Historical loss data that does not reflect current physical condition

Without post storm property condition verification, underwriting decisions are made on incomplete information. This increases the likelihood of mispriced risk and unexpected loss.

Residential vs Commercial Snow Risk in Insurance Underwriting

Snow risk presents differently across property types, requiring different underwriting considerations.

Residential Property Snow Risk Factors

Underwriting risk in residential portfolios often includes:

Ice dam formation leading to latent interior water damage

Excessive snow load on older or low slope roofs

Freeze thaw driven foundation and masonry cracking

Blocked vents increasing moisture and mold exposure

These conditions may not trigger immediate claims but significantly increase the probability of future loss.

Commercial Property Snow Risk Factors

Commercial properties introduce scale and operational complexity that amplify snow related exposure:

Flat roof snow accumulation exceeding design limits

Blocked roof drains causing ponding and membrane failure

Mechanical units buried or damaged, increasing business interruption risk

Site conditions elevating slip and fall liability

For underwriting teams, these risks cannot be inferred from desk reviews alone.

Post Event Property Condition Verification for Underwriting Teams

To close the visibility gap, underwriting and risk teams are increasingly incorporating post event property inspections into their workflows.

ProxyPics supports this by enabling on demand, on site property condition verification across residential and commercial portfolios. Data is collected by trained, background checked inspectors or through guided self enabled inspections, depending on portfolio needs.

Captured data focuses on underwriting relevant indicators, including:

Roof condition and visible snow load

Drainage performance and ice buildup

Mechanical and utility exposure

Site conditions affecting liability

All inspections are time stamped, standardized, and reviewed through quality control processes.

Using Machine Learning to Support Insurance Risk Assessment

ProxyPics applies machine learning to analyze photos for snow related risk indicators that matter to insurance underwriting teams.

This includes:

Flagging conditions associated with elevated loss probability

Identifying severity thresholds aligned with underwriting review criteria

Standardizing condition grading across large portfolios

Highlighting properties that warrant deeper review or mitigation

Machine learning supports consistency and prioritization without replacing underwriting judgment.

Scaling Portfolio Risk Reviews With Self Enabled Inspections

Snow events often impact wide geographic regions at once, making traditional field inspections difficult to scale.

Self enabled inspections allow underwriting teams to:

Rapidly verify post storm property conditions

Reassess exposure without waiting for field availability

Maintain standardized capture through guided workflows

When combined with machine learning validation and QC review, self enabled inspections provide underwriting teams with actionable data at portfolio scale.

Snow events expose the limits of static underwriting models. Insurance underwriting and risk teams that rely solely on desk reviews are making decisions without current property condition data.

Post storm, on site property condition verification provides the visibility underwriting teams need to assess real exposure, prioritize risk, and make defensible decisions in a changing environment.

If snow events are creating blind spots in your insurance underwriting or portfolio risk strategy, it may be time to introduce post event property condition verification into your workflow.

Talk with ProxyPics about on demand and self enabled inspections built for underwriting and risk teams.